BradNaylor

Established Member

- Joined

- 17 Oct 2007

- Messages

- 2,311

- Reaction score

- 2

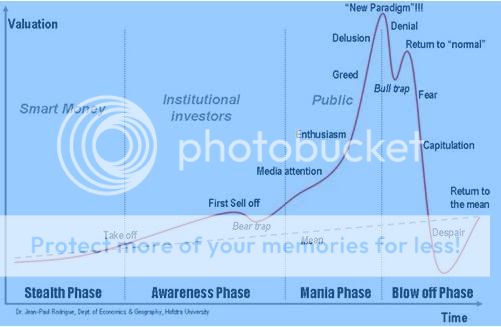

Builder chappy bought the 3-bed house across the road from us in early 2007 for a 'knockdown' £165k

He spent a year gutting the place, and building an extension which almost doubled the floor space and gave 5 bedrooms - 3 en-suite. He spent around £60k plus his own time. He showed me round and he's done a lovely job.

He put it up for sale in late 2007 for £299k despite my advice that the market was crashing and that the very most that any house in the neighouring area had sold for was £230k. I sugested he settle for £250k but was met with derision.

Yesterday he told SWMBO that he has finally sold it - for £205k. He is also delighted, as he expects the market to fall by another 25% over the next year or so.

I think he's right.

The difference a couple of years makes...

Brad

He spent a year gutting the place, and building an extension which almost doubled the floor space and gave 5 bedrooms - 3 en-suite. He spent around £60k plus his own time. He showed me round and he's done a lovely job.

He put it up for sale in late 2007 for £299k despite my advice that the market was crashing and that the very most that any house in the neighouring area had sold for was £230k. I sugested he settle for £250k but was met with derision.

Yesterday he told SWMBO that he has finally sold it - for £205k. He is also delighted, as he expects the market to fall by another 25% over the next year or so.

I think he's right.

The difference a couple of years makes...

Brad

") :wink:

:wink: